By William Jhanesta

Indonesia, already hosting four LNG plants with a combined capacity of 14.99 MTPA, is further advancing its offshore LNG production facilities to leverage its vast gas resources. In addition to expanding the current LNG capacity to over 35 MTPA through 16 planned new plants, efforts are underway to implement floating LNG (FLNG) technology.

After rejecting the proposal for the development of an FLNG plant for Indonesia's largest and most remote Abadi gas project within the Masela Production Sharing Contract (PSC) in 2016, the administration of President Joko Widodo has recently approved its use by a Malaysia-based upstream company for a smaller onshore gas field in West Papua. This approval signals a hopeful outlook for the development of additional FLNG projects in Indonesia.

The development of FLNG in the country would significantly contribute to meeting Indonesia's growing domestic gas needs, particularly for mineral smelter industries. LNG is positioned as a key strategy in their efforts to decarbonize the high carbon-intensive industry.

In this short article, we will discuss why Indonesia is suitable to be the home of FLNG development. Additionally, we will explore some announced projects that will implement FLNG plants. This analysis will also take a look at oil and gas blocks that have the potential and could be considered by operators for the development of offshore FLNG plants for gas monetization in the upcoming years.

Why FLNG fits with Indonesian gas fields?

Although no FLNG facilities are operational in Indonesia to date, Petromindo sees Indonesia as having significant opportunities for the development of offshore liquefaction facilities due to several considerations.

The first and foremost factor is cost-effectiveness. This is related to the fact that the construction of onshore LNG plants requires a considerable footprint. This condition is accompanied by the rising cost of land, including the complex processes of land acquisition and permitting. There have been numerous cases in the country where project implementation was hindered by land-related issues.

In addition, the location of gas wells in Indonesia is predominantly offshore. It allows field operators to liquefy gas directly on a barge-based LNG plant, minimizing additional costs for building extra infrastructure to transport gas to the onshore, which can be challenging in some cases.

FLNG can be utilized to develop stranded offshore gas fields or a combination of gas fields with sufficient resources, which were previously considered commercially unviable for conventional onshore LNG liquefaction development due to their remote locations.

The development of FLNG also has the potential to reduce the construction costs of jetty associated with the LNG loading process from onshore production facilities to LNG carriers. With FLNG, the LNG loading process can be expedited, either through or without the need for a floating storage and regasification unit (FSRU).

Masela FLNG rejected amid domestic growth concerns

The Abadi gas field is located in the Masela PSC in the Arafura Sea, approximately 150 km southern part of Tanimbar Islands, Maluku Province. Exploration and appraisal activities have confirmed that the Abadi field contains significant gas and condensate reserves. However, due to its remotely-located deepwater setting, it requires a 180 km gas pipeline from the field to cross a 3,000 m deep trench, which is a significant technical challenge. Clearly, the monetization of this vast gas field presents considerable difficulties.

Given the challenging nature of the Abadi gas field's development, INPEX, the operator of the Masela PSC, opted to utilize FLNG as the method for monetizing the giant gas reserves. In December 2010, INPEX received approval for Plan of Development (POD)-1 for the Abadi field, outlining a FLNG plan with a capacity of 2.5 MTPA. Five years later, INPEX submitted a revised POD-1 to enhance the FLNG capacity to 7.5 MTPA.

However, following high-profile debates among cabinet members, President Joko Widodo in March 2016 instructed INPEX to develop the gas-rich Abadi field based on an above-ground production scheme, arguing that it would provide a greater multiplier effect for the country and the people of Maluku.

Following the change in the production scheme to an onshore LNG facility, INPEX requested a number of incentives to make the project commercially feasible. The request includes expanding the LNG production capacity to 9.5 MTPA.

Upcoming FLNG project

According to Petromindo’s LNG Database, there are at least three announced FLNG projects taking shape in Indonesia, with two located in Papua and one in East Java. Following the cancellation of the FLNG Masela project, the development of these three FLNG projects will serve as benchmarks for the construction of future national offshore liquefaction plants.

Kasuri FLNG project

Malaysia-based upstream oil and gas company and operator of Kasuri block, Genting Oil Kasuri Pte Ltd (GOKPL) announced in February last year that the Indonesian Ministry of Energy and Mineral Resources has approved the revision to the POD-1 for the Asap-Kido Merah (AKM) gas field.

Under the revised POD, the ministry has signed off on Genting supplying for 18 years of 230 MMSCFD to an FLNG, the first time offshore liquefaction plant will be used in Indonesian waters, while a further 101 MMSCFD will go to a USD 1.5 billion petrochemical plant to be built by state-owned fertilizer company PT Pupuk Kalimantan Timur on the south coast of Bintuni Bay in Birds Head region, Papua.

Following the approval, GOKPL announced that the FLNG plant will be developed by its wholly-owned indirect subsidiary PT Layar Nusantara Gas (PT LNG) under the downstream scheme, with a capacity of 1.2 MTPA.

In early September 2023, PT LNG and Chinese Wison Heavy Industry Co Ltd, an affiliate of Wison Offshore & Marine, entered into a limited notice to proceed agreement to purchase USD 43.04 million of long lead items, such as cold box, compressor, and generator sets.

However, Genting’s upstream experience is limited as it only owns a non-operated interest in an offshore field in China which will be its entry into the LNG value chain. Therefore, it will be a big task for Genting to take on the proposed AMK-to-FLNG development as an operator and on a 100% basis.

The most likely option for Genting would be to engage a third party with the expertise and know-how to bring this initiative into reality. Recently, an industrial source confirmed that Genting is in talks with local gas trading company PT Rukun Raharja Tbk (RAJA), where Genting will farm down its 20% interest to RAJA. In addition to that, RAJA will also acquire shares PT LNG, which seems to be a positive support for Genting's FLNG project.

The FLNG is projected to begin operations in the first half of 2026. Once operational, it will be the first FLNG facility in Indonesia and the second LNG plant to implement a downstream business scheme after the Donggi Senoro onshore LNG plant in Matindok, Central Sulawesi.

Madura FLNG project

Malaysian offshore services and infrastructure provider Bumi Armada Berhad recently announced the signing of a non-binding agreement with state-owned PT Pertamina International Shipping and gas trading PT Davenergy Mulia Perkasa to record key principles to develop and commercialize LNG from the Madura gas field within the Madura Strait PSC and its surrounding.

Pertamina may perceive the Madura region as a low-risk area for the development of its first FLNG facility in the country. This could serve as a strategic move to demonstrate their technological capabilities before venturing into the development of additional FLNG facilities in more remote areas.

By leveraging the expertise and experience of its potential consortium members, it is anticipated that Bumi Armada and Pertamina will design, engineer, construct, install, commission, hook-up, and operate a FLNG liquefaction and storage facility.

Bumi Armada added that preliminary discussions have been initiated with several potential off-takers and the first shipment of LNG is anticipated to take place three years after making the final investment decision (FID).

However, Husky-CNOOC Madura Limited (HCML), operator of the Madura Strait PSC, was not cited in the agreement. It is also not clear which volumes will support the potential vessel nor what market the gas will go to, as the three of the fields in the Madura Strait PSC (BD, MDA-MBH, and MAC gas fields) are already onstream with the production process at a floating production unit (FPU) and the gas delivered to the East Java market.

Canadian energy firm Cenovus Energy Limited and China’s CNOOC Southeast Asia Ltd each own 40% interest in HCML, with the remainder held by Indonesian independent Samudra Energy.

Mogoi Wasian FLNG project

PT Petro Papua Mogoi Wasian (PPMW), the operator of the Mogoi Wasian block, and two of its partners plan to develop a FLNG plant within the block. The PSC is located in Bintuni, West Papua Province, where there is no significant local gas demand.

PPMW had in September 2023 signed a memorandum of understanding (MOU) with offshore LNG infrastructure developer PT Jaya Samudra Karunia Gas (JSKG) and Hong Kong-based Tunhua International Group Co Ltd to realize the planned FLNG plant.

The company said the floating LNG plant will have a production capacity of 1.5 MTPA of LNG. The partners are targeting PLN's power plant market and the growing smelter industry in eastern Indonesia, with an estimated total investment of USD 2 billion.

State-owned upstream firm PT Pertamina EP (PEP) previously signed an agreement with PPMW in 2014, allowing the latter to develop the block.

Potential FLNG projects in the country

Following the three-announced FLNG projects in Indonesia, Petromindo observes that there are several other gas discoveries in the country that have the potential to be developed with a similar scheme, especially for some PSCs in Maluku, Natuna, and Aceh. Each location presents its own challenges in monetizing gas discoveries.

Seram (Non-Bula) PSC: Lofin field

Seram (Non-Bula) PSC is located onshore in Seram Island, Maluku Province, and spans an area of 1,524 sq km, covering a portion of the original Seram PSC following its expiry date in October 1999. The block is operated by China’s Citic Seram Energy Ltd.

Citic announced in February last year new gas reserves in the Lofin field within the PSC through re-testing of the Lofin-2 exploration well. According to SKK Migas, the Re-entry Lofin-2 well flows gas of 15.02 MMSCFD at 64/64 inch choke opening.

Being located on a remote island, however, makes the commercialization of the Lofin gas field quite a challenge as there is no significant local demand and no existing export infrastructure. This makes gas commercialization using an FLNG scheme a concept that Citic should consider.

Yet, the economic challenges for the operator to fund such an integrated project remain. In this context, Citic, along with its partner, the 2.5% participating interest holders, Lion Energy Limited, should consider the development of FLNG with a downstream business scheme.

Pertamina or other major LNG specialists could also participate by financing and owning the FLNG plant, following a similar scheme to what Pertamina is currently working on for its first FLNG project in Madura.

Eastern Natuna PSCs

The eastern part of Natuna has several oil and gas blocks and stranded gas fields that have not been commercialized due to infrastructure limitations, making their development risky and costly. In contrast, its western counterpart, already has a pipeline network with a diameter of 48 inches. This network starts at the West Natuna Sea (Indonesia) and extends to South West Singapore, spanning 656 km, known as the West Natuna Transportation System (WNTS).

According to Petromindo’s Upstream Database, there are currently 6 blocks within the East Natuna region, with two of them being stranded gas fields, including the giant gas field Natuna D-Alpha and Medco’s previously operated South Sokang.

The development of an FLNG vessel in East Natuna could be considered to unlock stranded resources in far-flung fields, especially as demand for gas rises, particularly for sales to the Asia-Pacific region. Various development schemes, including monetizing associated gas production from several small gas fields, could be considered, where the development of a single field may be deemed uneconomical.

In this context, an LNG merchant business scheme, where upstream and liquefaction facilities are owned by different companies, is likely the most suitable option. This scheme allows the operator to sell the gas to the FLNG vessel owner, with the liquefaction project earning revenue from selling the produced LNG.

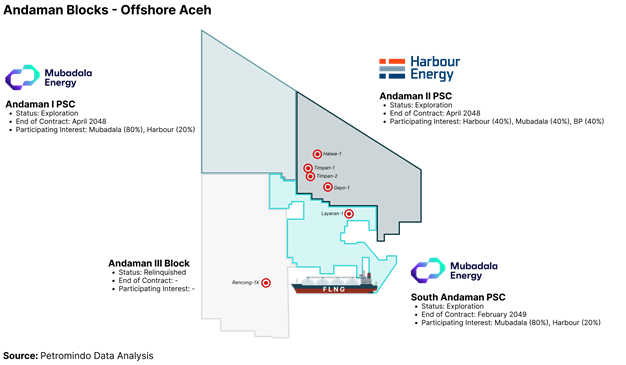

Andaman PSCs

The Andaman Sea has succeeded in being a global spotlight in the upstream business with the discoveries of Timpan-1 in 2022 and Layaran-1 in 2023. These discoveries serve as a play-opener for the Andaman frontier zone and show early promise for new development areas in the region. In recent articles, Petromindo expects that these two discoveries will be game-changers and have the potential to revitalize Aceh as the nation's energy hotspot.

UK-based Harbour Energy drilled in May 2022 the Timpan-1 exploration well into a total depth of 4,212 m in the Andaman II PSC at a water depth of close to 1,300 m. Guided by a bright flat spot from the previously acquired 3D seismic data, the well flowed on test at 27 MMSCFD of gas and 1,884 BOPD of condensate.

In December 2023, UAE-based Mubadala Energy announced a significant gas discovery from the Layaran-1 exploration well in the South Andaman PSC. Following the completion of data acquisition, including wireline, coring, sampling, and production test (DST), the well successfully flowed over 30 MMSCFD of excellent gas quality, as claimed by Mubadala. The company stated that the discovery has potential gas-in-place for more than 6 trillion cubic feet (TCF), marking a major development for the Southeast Asia energy landscape.

In addition to these two discoveries, Petromindo's recent analysis mentioned that the majority of Indonesian high-impact wells (HIW) in 2024 will mainly be focused on Andaman. Seadrill Limited’s West Capela drillship is currently undergoing vertical drilling of the Gayo-1 exploration well in Andaman II PSC, with a final planned depth of 11,733 ft. After Gayo-1, the rig will drill Halwa-1 located in the same block. Subsequently, it will return to South Andaman to drill the Layaran-2 well and other prospects.

While an onshore liquefaction plant in Arun seems to be the most likely option for monetizing the Andaman gas, other alternatives may include the deployment of a FLNG facility. This option is worth considering given that the Andaman blocks are situated in a frontier zone and deepwater area, similar to the conditions in the Abadi gas field. Implementing FLNG development in the Andaman region could follow a fully integrated route, involving collaboration between well-established firms Mubadala and Harbour Energy.

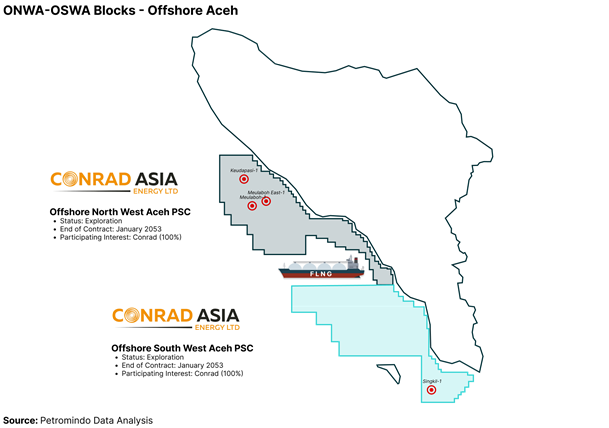

ONWA-OSWA PSCs

Offshore North West Aceh (ONWA – Meulaboh) and Offshore South West Aceh (OSWA – Singkil) PSCs are situated in offshore Northwest Sumatra. Conrad Asia Energy and the Aceh upstream oil and gas authority BPMA formally signed the sharing contract at the beginning of 2023.

Both blocks contain gas discoveries made in the 1970s. Back then, these finds were deemed uncommercial due to the lack of mature gas markets. Conrad has identified 38 leads in the two offshore blocks containing combined prospective resources over 15 TCF of recoverable gas.

A news headline popped up recently that Conrad is commissioning an independent study to identify and evaluate commercialization for the discovered gas resources at the two offshore blocks. The company is likely considering the development of an above-ground LNG plant with a capacity to process 25-30 MMSCFD of gas.

Given its relatively modest capacity, however, there is no reason to rule out the consideration of FLNG. As a point of reference, Malaysia-based Petronas currently operates FLNG Satu offshore Sarawak with a capacity of approximately 1.2 MTPA. This vessel became the world's first on-stream FLNG facility in 2017.

However, since its entire upstream assets in the country are still in the exploration-development stage and none of them have yet been monetized, the company is likely to face challenges in securing the necessary financing for the construction of the LNG plant.

The successful development of FLNG in ONWA-OSWA hinges significantly on the divestment process in the Duyung PSC. Conrad is reportedly exploring the option to farm down its 24% interest within the block, reducing its current 76.5% participating interest. The gas output anticipated from the Mako discovery within the Duyung PSC will most likely be supplied to Singapore via pipeline.

Another viable option for Conrad is to seek a financially robust LNG company as a partner for the collaborative construction and ownership of the FLNG plant, mirroring a similar concept proposed for the FLNG development in the Seram (Non-Bula) PSC. This strategic partnership would not only alleviate financial burdens but also bring in expertise and resources crucial for the successful realization of the FLNG project.